Tackle CFO challenges to accelerate your business impact.

- Gartner client? Log in for personalized search results.

Succeed as a New CFO

Recommendations for new CFOs in transition

Starting a new CFO role can be one of the most stressful, yet rewarding, career milestones. Here’s a guide to get you started on the right trajectory.

Explore Gartner’s best-practice insights from new-to-role and tenured CFOs and learn how to:

Take a structured, purposeful approach to your new role

Navigate the overwhelming number of competing tasks during your first few months in the role

Use a four-step approach to execute against priorities: prepare, connect, assess and act

New CFOs: A roadmap to success

It’s critical for new CFOs to manage a range of early responsibilities effectively to make their mark and drive value to the organization.

- Prepare

- Connect

- Assess

- Act

Prepare to mitigate context-related risks that can make or break your transition

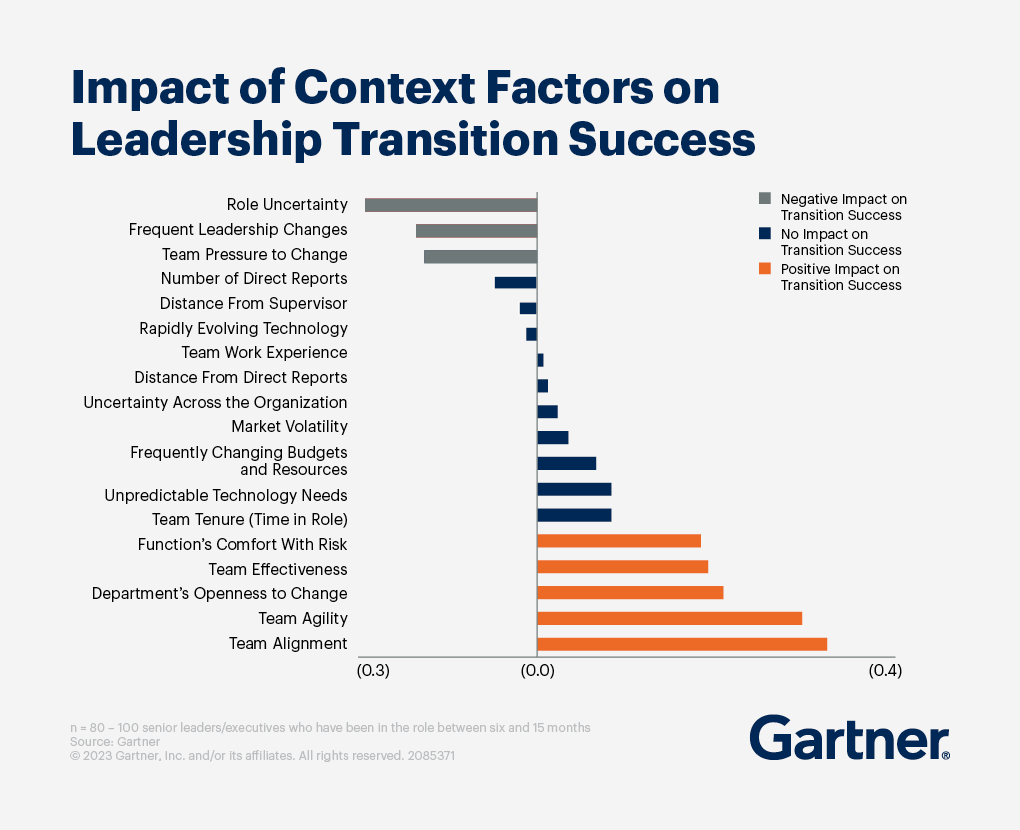

Gartner research indicates that CFOs’ context can have a direct impact on their performance. There are factors, such as change aversion and uncertainty and team agility and alignment, that can make or break a transition. New CFOs must understand the contextual factors that can impact their performance and proactively plan to address them or account for them.

Preparing for your CFO transition includes:

Mitigating team change aversion

Minimizing team change uncertainty

Facilitating team agility and alignment

Mitigating team change aversion

Our analysis shows there is a negative relationship between pressure on teams to change and new CFO performance. The greater the volume and scale of change the new CFO needs to drive, the higher the probability that finance team performance targets will be missed. But not everything related to change is negative: If the incoming CFO joins a team that is comfortable with risk and open to change, the chances that the new leader will succeed increase. In fact, the higher the team’s risk tolerance or openness to change, the larger the positive impact on new leaders’ performance.

The best way to accomplish this is through an “open change” approach. This harnesses the power of the broader finance team to collaborate, create and implement change — ultimately driving employee excitement and buy-in. In fact, when an organization uses an open change strategy, the probability of change success increases by as much as 24%. The defining characteristics of an open change approach are:

Co-create change strategy with employees, don’t just dictate it.

Enable employees, not just their managers, to own implementation planning.

Focus change communications on talking with employees, instead of just telling them about it.

Minimizing team change uncertainty

CFOs must help their teams navigate change uncertainty, which negatively affects engagement and productivity. The best way to do this is by making their teams feel empowered in the following ways:

Provide teams with support, not just directives.

Create an environment where finance employees feel they can innovate and experiment and be comfortable with risk taking.

Connect with employees so they can get the answers and resources they need.

Actively seek feedback from employees.

Facilitating team agility and alignment

Finance work is highly dependent on collaboration and coordination with others. As such, new CFOs must consider how their teams connect with other stakeholders, and understand the trade-offs between agility and alignment. This needs to be on new leaders’ radar even before they get into their new roles, as Gartner research shows these two factors really do matter and lead to more successful CFO transitions.

Team agility is the ability to quickly understand new business contexts and change how finance works to provide the most value for the organization. While CFOs can make a number of changes to improve their function’s agility, these are the most common and successful approaches:

Master transactional, day-to-day activities and processes.

Break down silos by integrating finance teams.

Rethink talent strategy to continuously adapt to changing internal and external environments.

Boost analytics capabilities to respond to new business requests.

Upgrade processes to more flexible approaches.

Build relationships.

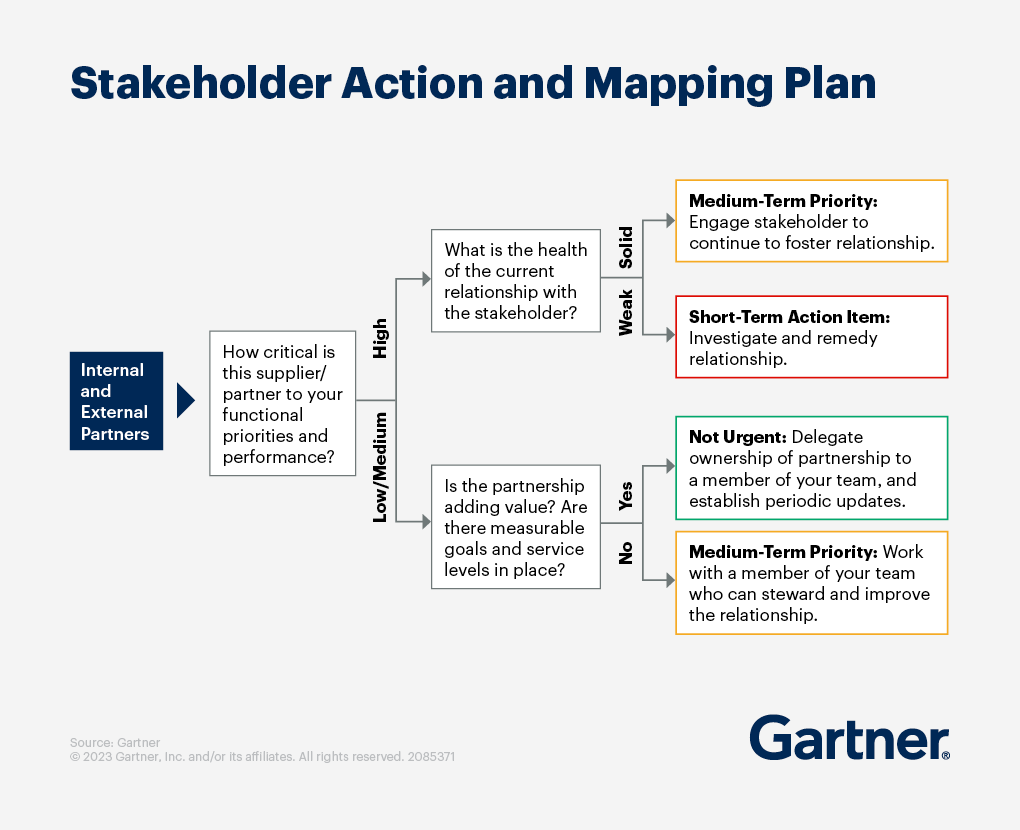

Build stakeholder relationships based on trust

Successful CFO transitions are about building relationships and trust and establishing credibility. Doing so with your peers, the C-suite and the board is particularly important.

Gartner research indicates that new executives who intentionally yet quickly build a strong network among company leaders are 50% more likely to succeed in their transitions.

Connecting during your CFO transition includes:

Building stakeholder relationships

Building team trust

Establishing your personal brand

Building stakeholder relationships

As work becomes more complex and collaborative, new executives’ success becomes more dependent on colleagues in other functions. To influence the performance of employees outside the executive’s reporting line, relationships with the board, CEO and peer executives are critical.

Incoming CFOs need an intentional, not instinctive, approach to relationship building. Our research identifies the principles new CFOs can follow to increase the likelihood of building an internal network that has a net-positive effect on their performance:

Prioritize stakeholder relationships.

Build relationships based on credibility.

Clarify boundaries and expectations.

Building team trust

An important component of new CFOs’ success is the team they manage. CFOs’ direct reports can arm them with information about the workings of the organization; help them understand finance’s strengths, weaknesses, opportunities and threats; and provide a sounding board. But direct reports may be apprehensive about the new CFO, depending on their relationship with the previous CFO and their own career interests and ambitions.

When new CFOs are build trusting relationships with their new direct reports, their teams must feel comfortable providing proactive upward coaching and feedback. CFOs can follow these principles to build team trust:

Focus on getting to know each direct report individually. Ask about their motivators and work challenges, and seek their feedback about the team.

Communicate expectations to employees of what level of value they should bring to the various activities they work on.

Involve the team in assessments, key decisions and goal setting, where appropriate.

Foster an environment of team development.

Establishing your personal brand

A personal brand is your reputation, what you are known for and what people think about you. What type of CFO are you considered to be? The tech-savvy CFO? The disruptive CFO? The growth-guru CFO? A brand communicates your purpose, establishes credibility and creates hype — helping you connect with stakeholders in the new company. New CFOs who don’t build a brand will have one created for them, and it may be less than flattering.

Incoming CFOs should use the following checklist to see if they are on track in developing and managing their personal brand:

What is your current reputation for execution, leadership, vision and innovation?

What is your target brand in three words or less, and how will you know when you have achieved your brand ambition?

What key events are milestones for your brand (for example, a board review)?

What stakeholder relationships need to be nurtured (upward, downward and horizontally)?

How will your personal brand contribute to the enterprise mission?

Benchmark your function’s maturity level to drive stretch performance

For internal CFO hires, assessing the current state of the function throughout the enterprise may only require a light touch or a drill-down into known areas of opportunity. If the transitioning CFO is an external hire, assessing presents both a challenge and opportunity. Review available performance data, benchmarks and feedback surveys to analyze and understand the key issues to address and establish a clear set of initial priorities. Avoid analysis paralysis. Gain insight, and refine over time.

We suggest the following assessment breakdown:

Assessing finance performance, costs, process maturity and alignment

Assessing your talent profile

Assessing organization design

Assessing finance performance, costs, process maturity and alignment

Finance leaders struggle to define a clear and comprehensive understanding of their function’s effectiveness, leaving them with the wrong priorities, unfocused investments and unsupported initiatives. To avoid this pitfall, new CFOs should assess their organization to identify opportunities to improve performance and efficiency in these four categories:

Performance: Understand how major facets of the finance function are performing.

Costs: Analyze personnel, technology, overheads and any other costs necessary to the operation of the finance function.

Process maturity: Determine how advanced the finance function’s capabilities are relative to other organizations. With finite resources, CFOs have to prioritize the capabilities that matter most.

Alignment: Understand which activities matter most to internal stakeholders and stakeholders’ perception of the value of finance’s support for those activities.

Assessing your talent profile

Knowing how well the organization’s current talent pool can meet current and future business needs is a priority for most transitioning CFOs. New CFOs should start a regular cadence to self-assess their function’s skills and competencies as part of updating the talent plan and investing in the development of the team. Keep these five recommendations in mind to assess current and potential talent:

Align talent expectations with business objectives.

Identify appropriate competencies to evaluate finance talent.

Clearly articulate competencies.

Identify proficiency and growth potential of current talent.

Proactively account for possible skill shortages.

Assessing organization design

Despite making changes to their finance functions’ organizational structures, even tenured CFOs continue to struggle to organize finance in a way that supports its efficiency and value-creation mandate. The best finance organizations choose structures based on how actual work is performed rather than rely on standard templates. New CFOs should consider the following to help accomplish this:

Centralization versus decentralization: Evaluate finance service delivery models — including corporate finance center, COE, shared services organization (SSO) and BU- or regionally aligned finance — based on your objectives.

Sourcing: To determine an outsourcing strategy, consider factors such as contribution to competitive advantage and impact on day-to-day operational performance.

Finance subfunction structure: Categorize the scope of finance subfunctions as narrow or broad, then think about their pros and cons in terms of costs of internal coordination, opportunities for specialization, agility and responsiveness, and customer experience.

Act to address the most pressing issues while paving a vision for the future

Establish a strategic vision and update the roadmap

New CFOs should set out a clear, forward-looking vision for the function early to help the team picture where the function is headed and how each individual role will contribute to team and business outcomes. Without a vision the team may lose focus, as employees’ mental energy and actions may not align with the new CFO’s ambitions — ultimately reducing productivity.

New CFOs should also make it clear how to accomplish the vision. Create a roadmap that mobilizes executive leadership, employee activity and resources against the initiatives that drive strategic execution.

At a minimum, a useful roadmap addresses these four themes:

Finance talent and knowledge: What is required to achieve the finance function’s vision? Does the function need new skills or simply to retain its high performers?

Finance process and policy: Do current processes and controls need to be broken to achieve the vision? If so, which ones and how? For example, does transactional efficiency need to be sacrificed to support higher-value judgment decisions?

Finance technology and data: What IT changes are needed to succeed? Does finance need to break down data silos to access new data or find new tools to improve the delivery of management reports?

Finance decision support: What are the roles of finance’s business partners? Does finance have to provide more accurate, timely reporting to existing constituents, or do new relationships need to be formed to accomplish the vision?

Identify potential functional risks

Meeting finance’s objectives is contingent on identifying, and addressing, risks in a timely manner. While risks to the CFO’s vision can vary greatly, keep these common ones foremost in mind:

New business requirements

Cost and efficiency demands

Technological disruption

Governance and risk

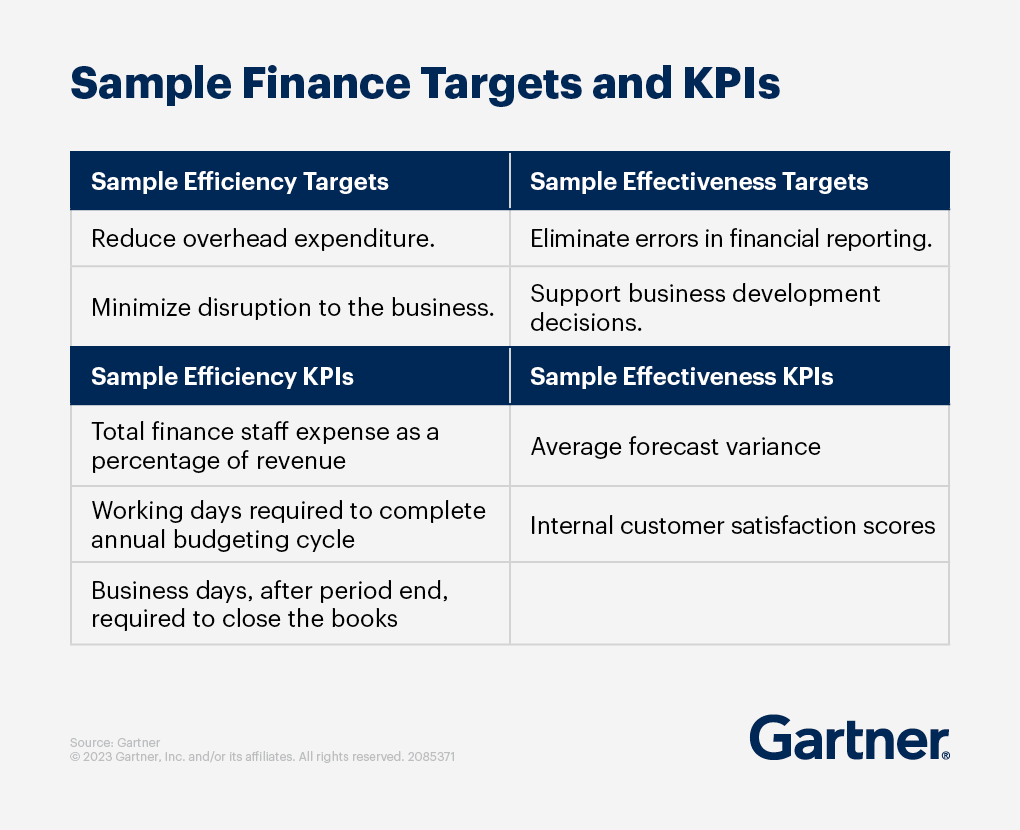

Measure improvement

The new CFO should support the vision with a set of aspirational but realistic performance targets, and KPIs to measure them. Set a combination of functional efficiency and effectiveness targets that, when executed well, drive the desired outcomes.

Gartner CFO & Finance Executive Conference

Join CFOs and finance executives to learn how to navigate emerging trends and challenges. From peer-led sessions to analyst one-on-ones, you'll leave ready to tackle your mission-critical priorities.

Related resources

{kind=link}

{kind=link}

{kind=link}

{kind=link}

FAQ on starting a new CFO role

What is the new CFO checklist?

The new CFO checklist includes:

Mastering the role and managing key relationships

Defining a vision for the function

Focusing on critical activities

Assessing staff capabilities

What makes a great CFO?

Great CFOs encourage behaviors required to drive profitable growth and deliver on their CEO’s expectations for financial performance.

How can CFOs navigate uncertainty and drive business goals?

CFOs must focus on how to:

Lead finance transformation and organizational change initiatives

Develop and refine the data and analytics strategy

Align spend to growth

Improve finance staff engagement

Define finance’s technology strategy and roadmap

Where should new CFOs focus to create an impact?

To be effective today, CFOs must focus their time and energy on initiatives that will deliver impact on critical strategies, such as improving the returns from digital bets for the organization and digitalizing the finance function itself.

Drive stronger performance on your mission-critical priorities.